When buying a home, you probably know many potential risks, such as the risk your home will go down in value over time or the risk that your home will require a lot of maintenance after purchase. In the same way, knowledgeable investors are aware that investing in the capital markets presents any number of risks – interest-rate risk, company risk, and market risk. Risk is an inseparable companion to the potential for long-term growth. Some of the investment risks we face may be mitigated through diversification, but not every risk can be diversified away. 1

When buying a home, you probably know many potential risks, such as the risk your home will go down in value over time or the risk that your home will require a lot of maintenance after purchase. In the same way, knowledgeable investors are aware that investing in the capital markets presents any number of risks – interest-rate risk, company risk, and market risk. Risk is an inseparable companion to the potential for long-term growth. Some of the investment risks we face may be mitigated through diversification, but not every risk can be diversified away. 1

As an investor, however, you may face another, lesser-known risk that diversification may not easily reduce. Yet, it may be one of the biggest challenges to the sustainability of your retirement income. What is this risk? It is known as sequencing risk.

Sequencing Risk Explained

Sequencing risk is the uncertainty regarding the sequence of returns over time. To better understand sequencing risk, consider this example of a fictional couple named John and Jane Moneysaver.

Over the first 25 years of retirement, the Moneysavers’ average return was 5% per year. While their average return was positive over this 25-year period, unfortunately, John and Jane lost money on their investments for the first 10 years of their retirement. The Moneysavers, in effect, realized some significant sequencing risks as the sequence of their returns were negative before they turned positive later in retirement.

What if the Moneysavers needed $50,000 a year before taxes from their portfolio to meet their living expenses and had a total savings of $1 million? To meet these expenses, this couple would need average returns of at least 5% per year. If their returns were negative during their first 10 years of retirement, they would most likely have been spending from principal to cover their spending needs. As a result, the projected value of their portfolio would have been considerably smaller after 10 years of retirement compared to a sequence of positive 5% returns for the first 10 years of retirement.

Averages matter over time, but what may matter even more are the actual returns that make up the averages. As Milton Friedman once observed, you should “Never try to walk across a river just because it has an average depth of four feet.” 2

Mr. Friedman’s point was that averages may hide dangerous possibilities. This is especially true with the stock market. You may be comfortable that the market will deliver its historical average return over the long term, but you can never know when you will be receiving the varying positive and negative returns that comprise the average. The order in which you receive these returns can make a big difference.

For instance, if history is any guide, a market decline of 30% or more during any decade is not to be unexpected. However, would you rather experience this decline when you have relatively small retirement savings or are ready to retire – when your savings may never be more valuable? Without a doubt, the former scenario is preferable, but the timing of that large potential decline is most likely out of your control.

The sequence-of-returns risk is especially problematic while you are in retirement. Down years, combined with portfolio withdrawals taken to provide retirement income, can seriously damage your savings’ ability to recover sufficiently even as the markets fully rebound.

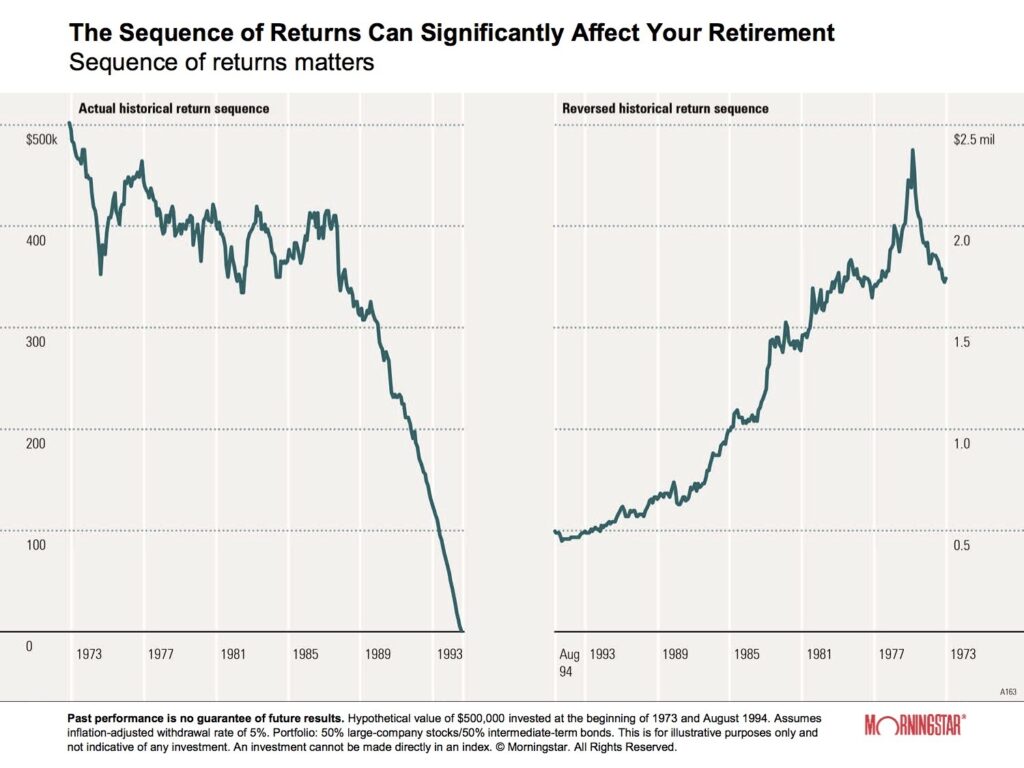

This Morningstar chart shows a hypothetical value of $500,000 (50% large company stocks and 50% intermediate-term bonds) invested at the beginning of 1973 until August 1994, with an inflation-adjusted withdrawal rate of 5%. It illustrates just how much your retirement could be affected by the sequence-of-returns risk. What if you could go backward in time and start your retirement in 1994 and work your way back to 1973, as the chart to the right illustrates? The returns each year would have been identical to the chart on the left, but because your sequence of returns was mainly positive in the beginning, the projected value of the portfolio would have been higher in this hypothetical example.

What are some things you can do today to help create an income cushion and reduce your sequencing risk during your retirement?

Plan for Risk

As you consider your options, keep in mind that a certain amount of risk is unavoidable. Diversification may be helpful, to a degree, but it may also be helpful to have an income-generating plan in mind if you face a difficult year ahead.

Investment Strategy – You may be tempted to place money into risky and speculative investments to increase your portfolio’s return potential. Rather than risk big losses you have little time to recover from, save reasonably and call us to discuss a balanced investment approach that can help address sequencing risk.

Work Longer – Are you able to delay retirement for a year or more, potentially adding additional years to your savings as well as allowing for the financial environment to recover? If so, we recommend you consider this option and create a financial plan to better define your actual needs. If you need help with planning, call us, and we’ll be happy to either create a plan for you or make some planning suggestions.

Other Alternatives – Some other alternatives may be to reconsider, downsize, or delay some of your bigger plans to save more. These alternatives may not be preferable, but you can take comfort in having those plans and ideas in place should they ever become necessary. As with the previous suggestion, we recommend creating a financial plan to better define your needs.

CITATIONS:

About The Goff Financial Group: As a fully independent Registered Investment Advisor, the Goff Financial Group is not owned or controlled by any bank, brokerage firm, mutual fund company or any other company. The company does not receive any fees or commissions from any financial products and works solely for its clients on a fee-only basis. Disclaimer: This material was prepared using third party resources, and does not necessarily represent the current views of The Goff Financial Group which are subject to change without notice. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering tax or legal advice. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as financial, investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This document is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.